Excellent perspective Dr Cooper!

|

|||||||

|

General Bob Rees 22 Jun

Excellent perspective Dr Cooper!

|

|||||||

|

General Bob Rees 16 Jun

Some more GOOD NEWS! Thank you Dr Cooper 🙂

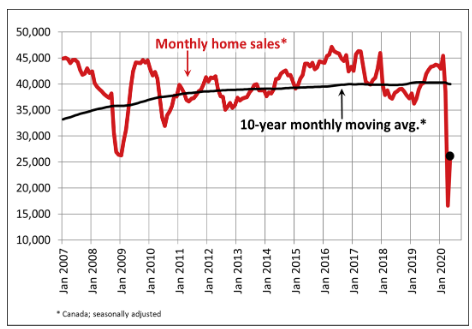

There was good news today on the housing front. Home sales surged by a record 56.9% in May from April’s unprecedented collapse. Data released this morning from the Canadian Real Estate Association (CREA) showed national home sales recovered roughly one-third of the COVID-induced loss between February and April (see chart below). On a year-over-year (y-o-y) basis, sales activity was still down almost 40%, but the jump in sales and an even larger surge in new listings shows pent-up demand remains for housing as buyers wish to take advantage of historically low mortgage rates.

Transactions were up on a month-over-month (m-o-m) basis across the country. Among Canada’s largest markets, sales rose by 53% in the Greater Toronto Area (GTA), 92.3% in Montreal, 31.5% in Greater Vancouver, 20.5% in the Fraser Valley, 68.7% in Calgary, 46.5% in Edmonton, 45.6% in Winnipeg, 69.4% in Hamilton-Burlington and 30.5% in Ottawa. Not surprisingly, the cities with the smallest gains posted the smallest declines in prior months.

More importantly, anecdotal data suggest that housing activity has been steadily rising from the middle of April until the first week in June.

The number of newly listed homes shot up by a record 69% in May compared to the prior month with gains recorded across the country.

With new listings having recovered by more than sales in May, the national sales-to-new listings ratio fell to 58.8% compared to 63.3% posted in April. While this statistic has moved lower, the bigger picture is that this measure of market balance has been remarkably stable considering the extent to which current economic and social conditions are impacting both buyers and sellers.

There were 5.6 months of inventory on a national basis at the end of May 2020, down from 9 months in April. The temporary jump in this measure recorded in April reflected the fact that sales were expected to fall right away amid lockdowns; whereas, other variables like active listings would be expected to fall at a much slower pace. The CREA report suggests many sellers who already had homes on the market before mid-March may have left the listings up for now but drastically curtailed the extent to which they were showing their homes during the lockdown. With many of those now coming off the market, overall active listings have fallen by about a quarter as of the end of May, bringing them down among the lowest levels on record for that time of the year.

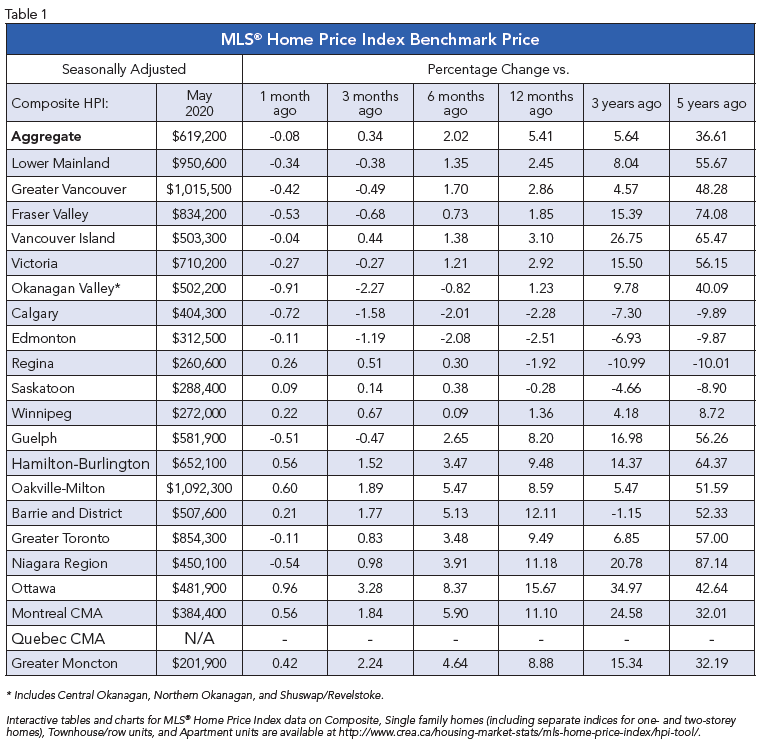

Home prices were little changed in May compared to April across Canada. Of the 19 markets tracked by the MLS Home Price Index (HPI), 18 recorded either m-o-m increases or smaller decreases than in April. Five markets posted price gains in May following a decline in April (see the table below for local details).

In general, since the pandemic crisis began small declines in prices have been posted in British Columbia while declining trends already in place in Alberta have accelerated. With the recent surge in oil prices, however, sales activity has actually improved across the Prairies and price trends have been stabilizing.

Despite the pandemic, home prices in the Greater Golden Horsehoe area around and including Toronto have fallen very little and remain well above year-ago levels. In Ottawa, Montreal and Moncton, prices have continued to climb, albeit at a slower pace than before.

CMHC has recently forecast that national average sales prices will fall 9%-to-18% in 2020 and not return to yearend-2019 levels until as late as 2022. I continue to believe that this forecast is overly pessimistic. Firstly, average sales prices are highly misleading, especially on a national basis because they vary so much depending on the location of the activity, as well as the types of property sold.

There is no national housing market. All housing markets are local. A glance at Table 1 above shows a wide variation in regional sales price action, but if anything, trends appear to be converging on moderate positive pressure on prices. Today’s economic recession is like no other. The record stimulus introduced by the Bank of Canada and the federal government will assure that the housing markets will continue to function, even with social-distancing measures in place, and those who enjoy steady employment will proceed in due course with regular housing decisions.

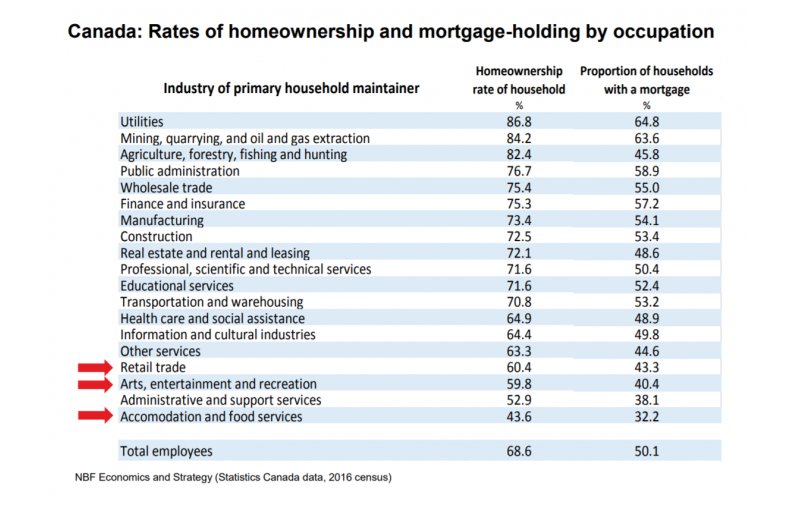

Those who permanently lose their jobs are the real concern. Many of those people will be in the hardest hit and slowest-to-recover sectors of our economy, such as hospitality (accommodation and food), non-essential retail trade, and the leisure industry (arts, entertainment and recreation). Statistics Canada census data for 2016 in the table below, shows that the homeownership rate in these sectors is relatively low. Unfortunately, most of those who will be hardest hit by the pandemic can least afford it. This is an issue that fiscal policy must address, investing in retraining programs and universal income guarantees.

General Bob Rees 8 Jun

This is a relief!

TORONTO, June 8, 2020 /CNW/ – Genworth MI Canada Inc. (the “Company“) (TSX: MIC) confirms that it has no plans to change its underwriting policy related to debt service ratio limits, minimum credit score and down payment requirements. One of the Company’s competitors announced changes to their internal underwriting guidelines with respect to the aforementioned underwriting criteria on June 4, 2020.

“Genworth Canada believes that its risk management framework, its dynamic underwriting policies and processes and its ongoing monitoring of conditions and market developments allow it to prudently adjudicate and manage its mortgage insurance exposure, including its exposure to this segment of borrowers with lower credit scores or higher debt service ratios,” said Stuart Levings, President and CEO.

SOURCE OF ABOVE:

General Bob Rees 7 Jun

I LOVE positive information! Thank you Dr Cooper 🙂

|

|

|

|

|

|

|

|

|

|

|

|

General Bob Rees 4 Jun

RULE UPDATE

HUGE CHANGE COMING FOR BUYERS ….. CMHC has made the below change effective July 1, 2020 .. if you or someone you know is buying with less than 20% down … this will reduce the amount you can borrow. The average impact will be a 14-15% REDUCTION in maximum purchase price!

SAMPLE IMPACT:

$300,000 Max Purchase Price today

$260,000 Max Purchase Price after July 1st

RULE CHANGE:

* Limiting the Gross/Total Debt Servicing (GDS/TDS) ratios to our standard requirements of 35/42;

* Establish minimum credit score of 680 for at least one borrower; and

* Non-traditional sources of down payment that increase indebtedness will no longer be treated as equity for insurance purposes.

I am here if any questions arise.

Cheers,

Bob Rees

Mortgage Broker

Powered by Maximal Mortgages and Dominion Lending Centres DLC

Call/Text: 780-975-9747

General Bob Rees 3 Jun

Thank you Dr Cooper …. happy to hear some “positive” info for a change 🙂

|

|

General Bob Rees 3 Jun

The Bank of Canada today maintained its target for the overnight rate at the effective lower bound of ¼ percent. The Bank Rate is correspondingly ½ percent and the deposit rate is ¼ percent.

Incoming data confirm the severe impact of the COVID-19 pandemic on the global economy. This impact appears to have peaked, although uncertainty about how the recovery will unfold remains high. Massive policy responses in advanced economies have helped to replace lost income and cushion the effect of economic shutdowns. Financial conditions have improved, and commodity prices have risen in recent weeks after falling sharply earlier this year. Because different countries’ containment measures will be lifted at different times, the global recovery likely will be protracted and uneven.

In Canada, the pandemic has led to historic losses in output and jobs. Still, the Canadian economy appears to have avoided the most severe scenario presented in the Bank’s April Monetary Policy Report (MPR). The level of real GDP in the first quarter was 2.1 percent lower than in the fourth quarter of 2019. This GDP reading is in the middle of the Bank’s April monitoring range and reflects the combined impact of falling oil prices and widespread shutdowns. The level of real GDP in the second quarter will likely show a further decline of 10-20 percent, as continued shutdowns and sharply lower investment in the energy sector take a further toll on output. Decisive and targeted fiscal actions, combined with lower interest rates, are buffering the impact of the shutdown on disposable income and helping to lay the foundation for economic recovery. While the outlook for the second half of 2020 and beyond remains heavily clouded, the Bank expects the economy to resume growth in the third quarter.

CPI inflation has decreased to near zero, as anticipated in the April MPR, mainly due to lower prices for gasoline. The Bank expects temporary factors to keep CPI inflation below the target band in the near term. The Bank’s core measures of inflation have drifted down, although by much less than the CPI, and are now between 1.6 and 2 percent.

The Bank’s programs to improve market function are having their intended effect. After significant strains in March, short-term funding conditions have improved. Therefore, the Bank is reducing the frequency of its term repo operations to once per week, and its program to purchase bankers’ acceptances to bi-weekly operations. The Bank stands ready to adjust these programs if market conditions warrant. Meanwhile, its other programs to purchase federal, provincial, and corporate debt are continuing at their present frequency and scope.

As market function improves and containment restrictions ease, the Bank’s focus will shift to supporting the resumption of growth in output and employment. The Bank maintains its commitment to continue large-scale asset purchases until the economic recovery is well underway. Any further policy actions would be calibrated to provide the necessary degree of monetary policy accommodation required to achieve the inflation target.

Tiff Macklem assumes his role as the Bank’s tenth Governor today. He participated as an observer in Governing Council’s deliberations for this policy interest rate decision and endorses the rate decision and measures announced in this press release.

The next scheduled date for announcing the overnight rate target is July 15, 2020. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

General Bob Rees 29 May

| Thank you for the insight Dr Cooper. I personally appreciate her positive view on CMHC’s most recent press release as its does appear the market is bouncing back and that the initial “drops” are not as significant as originally expected …. still drops just the same, but we are a strong and resilient bunch!

|

|

|

|

|

|

|

|

|

General Bob Rees 19 May

Great to see how one of our preferred lenders is managing the new World that COVID19 has presented, keep up the great work First National!

|

|||

|

General Bob Rees 15 May

Sales are still happening and there is activity … just less of it. Here’s to hoping the market rebounds as quickly as it dropped. See below from Dr Cooper. Cheers!

|

|

|

|

|

|

|

|

|

|

|